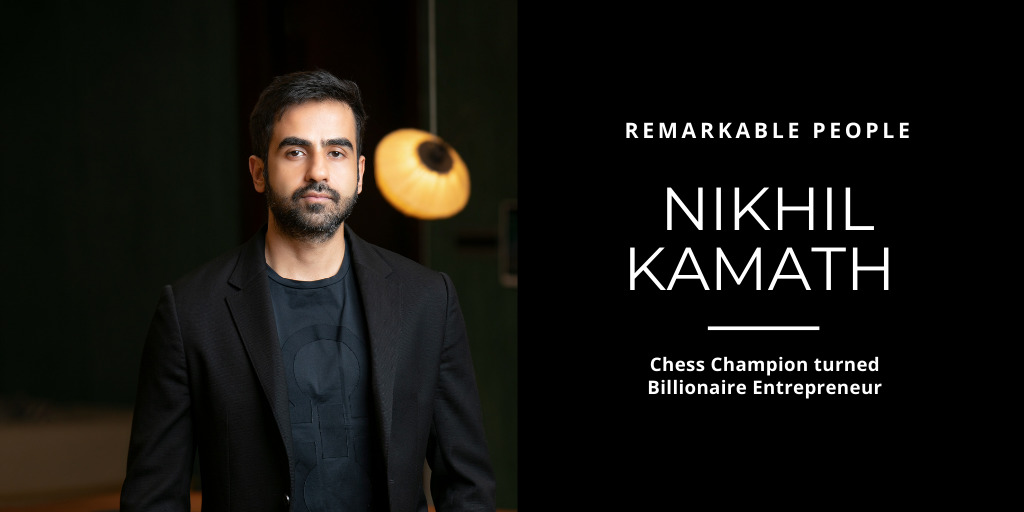

I’m Guy Kawasaki, and this is Remarkable People. Today’s guest is Nikhil Kamath, the co-founder of India’s largest stock brokerage, Zerodha.

For what it’s worth, he’s in his early thirties and a billionaire based on his stake in the company.

His “made for movies” story is that he dropped out of high school to play chess, worked at a call center answering support questions, started a stock brokerage, and became a billionaire. Kind of a Queen’s Gambit meets Slumdog Millionaire meets Charles Schwab.

But the actual storyline is not as Bollywood as you might think. The real value of this episode is his insights regarding:

- The value of removing barriers as a reason to start a company

- Methods of monetization in an industry where almost every service is free

- The advantages of not raising venture capital

- Using sentiment and psychology to make investment decisions

- The pitfalls of cryptocurrency

- The good and bad of a calm demeanor

Listen to remarkable Nikhil Kamath on Remarkable People:

I will be live streaming on April 7th at 10 am PT, watch then or catch the replay.

I hope you enjoyed this podcast. Would you please consider leaving a short review on Apple Podcasts/iTunes? It takes less than sixty seconds. It really makes a difference in swaying new listeners and upcoming guests.

Sign up for Guy’s weekly email at http://eepurl.com/gL7pvD

Text me at 1-831-609-0628 or click here to join my extended “ohana” (Hawaiian for family). The goal is to foster interaction about the things that are important to me and are hopefully important to you too! I’ll be sending you texts for new podcasts, live streams, and other exclusive ohana content.

Connect with Guy on social media:

Twitter: twitter.com/guykawasaki

Instagram: instagram.com/guykawasaki

Facebook: facebook.com/guy

LinkedIn: www.linkedin.com/in/guykawasaki/

Read Guy’s books: /books/

Thank you for listening and sharing this episode with your community.

Guy Kawasaki: Guy Kawasaki: Completely aside, just I'm interested in you as a person. How and when and what circumstances do you do your best and deepest thinking? The definition of stoic is someone who can endure hardship and pain without displaying their emotions or complaining. My impression of Nikhil is he is truly a stoic. This is Remarkable People.

Enter your name and email address below and I'll send you periodic updates about the podcast.

I'm Guy Kawasaki, and this is Remarkable People. Today's remarkable guest is Nikhil Kamath. Nikhil is the co-founder of India's largest stock brokerage firm, Zerodha. If this sort of thing impresses you, he's in his thirties and therefore one of India's youngest billionaires.

His made for movie story is that he dropped out of high school to play chess, worked at a call center answering support questions, started a stock brokerage and became a billionaire. Kind of a Queen's Gambit, meets Slumdog Millionaire, meets Charles Schwab.

But the actual store line is not as Bollywood as you might think. The real value of this episode is his insights regarding the value of removing barriers for people, methods of monetization in an industry where almost every service is free, the advantages of not raising venture capital, using sentiment and psychology to make investment decisions, the pitfalls of cryptocurrency and the advantages and disadvantages of a calm demeanor.

This episode of Remarkable People is brought to you by reMarkable, the paper tablet company. Yes, you've got that right. Remarkable is Sponsored by reMarkable. I have version two in my hot little hands and it's so good. A very impressive upgrade.

Here's how I use it. One: Taking notes while I'm interviewing a podcast guest. Two: Taking notes while being brief about speaking gigs. Three: Drafting the structure of keynote speeches. Four: Storing manuals for the gizmos that I buy. Five: Roughing out drawings for things like surfboards, surfboard sheds, and office layouts. Six: Wrapping my head around complex ideas with diagrams and flow charts.

This is a remarkably well-thought-out product. It doesn't try to be all things to all people, but it takes notes better than anything I've used. Check out the recent reviews of the latest version.

I'm Guy Kawasaki, and this is Remarkable People. Now here's the remarkable Nikhil Kamath.

Do you think that dropping out of school and playing chess really had any causative relationship with your success?

Nikhil Kamath:

It's an easy narrative to sell and people pick up on that and sell it. It might have had a small effect, but I don't think a really large effect, no.

Guy Kawasaki:

So you wouldn't advise kids to drop out and play chess in order to become a billionaire?

Nikhil Kamath:

Absolutely not. Especially in the startup universe. So few companies get lucky and they're in the right place at the right time, so would definitely not be their generic advice. No.

Guy Kawasaki:

I am actually more interested in if your experience working in the call center for a dollar a day had any causative relationship.

Nikhil Kamath:

Not as bad as a dollar a day, more like maybe five to $10 a day, back in the day.

Guy Kawasaki:

Okay.

Nikhil Kamath:

But the fact that you can't control the outcome in a call center when you're a cog in a really large wheel, I think leaves you feeling a little bit helpless and dependent on so many external factors and that definitely instigates you to want to take more control over what you're doing, so that definitely played a part. Yeah.

Guy Kawasaki:

For most Americans, if we have any appreciation of what happens in a call center, it's because of the movie Slumdog Millionaire. Most of us, when we call, I don't know, Quicken tech support, we're talking to somebody in Bangalore or Mumbai and we have no idea. So is it just rows and rows of people with headsets and you just pick up the phone and they start, "This is how you print a check on QuickBooks?"

Nikhil Kamath:

Yeah. The place where I worked at was called Twenty-Four/Seven Customer. I think I saw them grow from about a couple of a hundred people to many thousand people. So there would be three floors in a really large building with maybe three thousand people on the phone all the time.

Guy Kawasaki:

Wow. So that is a factory.

Nikhil Kamath:

Yeah. Yeah. Totally.

Guy Kawasaki:

Wow. So you started right after the financial crisis. So with hindsight, do you think that bad times create good companies?

Nikhil Kamath:

I think bad times create less competition. The fact that we started right after the financial crisis, I think there was very little capital going around, very little innovation in the industry by virtue of what had just happened. We kind of got lucky to be doing something new. We were in the right time at the right place and I think that helped significantly.

If we were to try and replicate what we did back then today it would be a lot harder because Fintech is the flavor of the season right now across the world and there is a lot of money and innovation chasing it.

Guy Kawasaki:

The name means zero barrier, I think. Let me verify that because you never know. So what barriers were you seeking to remove specifically?

Nikhil Kamath:

We were trading before becoming a broker. Back in the day, the incumbent brokers of then charged as much as half a percent of the total turnover of a transaction in broking fees. It made it very hard for a retail investor, trader to remain profitable because of all these leakages in the form of fee. So I think that's the barrier we faced as traders and that we tried to address as brokers. So that's what we were talking about at the very beginning, the cost and transparency element of it all was the barrier of the day.

Guy Kawasaki:

Does the creation of Zerodha reflect that it's fundamentally better to be the casino than to be the best gambler?

Nikhil Kamath:

I guess there is something to be said for both. Some of the best gamblers in the world have done very well and some casinos have also done well. I think two ways to look at the problem, but being a gambler is accelerating, being a casino is a bit more stable. So I think depending on what you're looking for, a different mode might suit you more.

Guy Kawasaki:

One story I read was that your brother was burned out as a trader, so then he wanted to go to the other side and be the casino. Is that a true story?

Nikhil Kamath:

Yeah, I think that is partly true.

Guy Kawasaki:

You make it coming and going, right? Doesn't really matter, does it?

Nikhil Kamath:

Yeah. But I think you make much less relatively to while you bet on something, if it works out, it really pays off. But while you're on the other side, you make small amounts of money many times, but there is a liability at hand. At some point, if somebody with a lot of leverage burns out, it goes into a debit or there is a technical glitch, both have their pluses and minus. I really don't think you can compare one with the other.

Guy Kawasaki:

But you certainly would not be worth a billion dollars as a trader.

Nikhil Kamath:

I know.

Guy Kawasaki:

I guess Warren Buffet is, but that's less likely, right?

Nikhil Kamath:

Yeah, true.

Guy Kawasaki:

Your trades are essentially free, but people pay for options, futures, and intraday trades. Is that because those things are harder to execute? Is it because there's price inelasticity because people are willing to pay for that? Or is it because that's the only three things that's left to charge people for since trading is free?

Nikhil Kamath:

The way the markets are structured in India, a lot of the volume, the speculation, actually comes from the derivative, the future option and intraday traders. So they form a large percentage of our overall clientele and they do pay a fee. They pay about twenty rupees per transactions, about one third of a dollar, vaguely, is how much they would pay to buy or sell any equity. We don't limit them with quantity. You could buy a million dollars’ worth of share X and you would only pay that one third of a dollar as fee. So that is our revenue model, essentially.

Guy Kawasaki:

Because you have to do that, because there's so many places you can "trade for free", but really the intraday... So you want intraday trading, you want thirty-three cents per transaction.

Nikhil Kamath:

That's right. So the intraday traders are essentially seventy percent of our volume and they do pay that fee. That fee to relative to the incumbents when we started is extremely cheap. It's ninety percent cheaper than anyone else charged when we began. The reason we have left equity investing as free is because India is a very large country. We have about a one hundred thirty-four people, and a very small proportion of India actually has financial exposure, something in the range of two percent.

Favorable taxation really helps long-term investors in India, they pay a much lower level of tax and capital gain if they have held the equity for over twelve months. So in a way, in order to encourage that, we have kept the equity investing part free and we hope more people will be long-term traders and allocate a certain portion of their asset base in the equity markets.

Guy Kawasaki:

Do you view that as a social responsibility because it doesn't help you to have long-term infrequent trades?

Nikhil Kamath:

I feel that if the ecosystem in the country grows, if a lot more people start allocating money to equity markets, A: I think it helps them diversify their portfolios, which right now in India we are too real estate bully and heavy in many ways. A lot of us leave money in a bank account which is badly beating inflation. So A, it affords people another asset class to diversify into. But B: if the ecosystem grows larger, I'm sure they will start trading. They will start doing other things where we do charge a fee… Sorry!

Guy Kawasaki:

Is that your ringtone?

Nikhil Kamath:

Yeah, it's the default one.

Guy Kawasaki:

A growing interest in the asset class will create people who will then dip into options, futures, and intraday trades. That's the thinking?

Nikhil Kamath:

Yeah. Yeah. The more people invest, I think the speculators also increase. I think that's a very natural correlation. People use it for hedging. A lot of people have equity portfolios, they want to buy insurance on it, they would come by a port option. A lot more savvy investors will come into the market and use the derivatives where we actually charge.

Guy Kawasaki:

How would you define your competitive advantage vis-a-vis the other brokers in India?

Nikhil Kamath:

I would say the ecosystem of products that we offer, I think that is the USP today. We have a lot of great technology around how you would analyze your portfolio, how you might back test, execution, the user interface - those are the reasons that people come to us today.

Guy Kawasaki:

Is that sustainable?

Nikhil Kamath:

To sustainably have the best? Maybe not, but we endeavor to kind of change as quickly as we can and put new stuff out there faster than the next guy.

Guy Kawasaki:

Do you have fractional shares?

Nikhil Kamath:

No, we don't. We don't.

Guy Kawasaki:

Obviously, that's the big deal with Robinhood, so why don't you have fractional shares?

Nikhil Kamath:

It's a regulatory thing. The Indian government, the regulator in India does not allow it.

Guy Kawasaki:

Are you lobbying for that change?

Nikhil Kamath:

Not really.

Guy Kawasaki:

No.

Nikhil Kamath:

Also I think you have many high value shares in America like you have before the split of Alphabet. Many companies which are creating at thousands of dollars, that is not the case in India here. Here, typically, stocks tend to split... the companies do it on themselves much earlier to keep stock prices in that range where people can still buy a share.

Guy Kawasaki:

My kids have Robinhood accounts and my interpretation of why they have that is because they may not be able to afford one share of Tesla, but now they think they're a Tesla shareholder because they own a fractional part of Tesla. Might be deceiving themselves, but that's the attraction. A lot of people, when I told them I'm talking to you, they said, "That's the Robinhood of India." But that's not at all true. Is it?

Nikhil Kamath:

No, it isn't.

Guy Kawasaki:

In the fractional sense.

Nikhil Kamath:

It isn't. It's actually not true in any sense because how a broker monetizes in America is very different from how one does it in India. Like Robinhood makes a huge portion of their revenue from things like selling order flow, and all of that is not allowed in India.

A broker is essentially a hop between a client and the exchange. All the order matching in India happens at the exchange level. Completely different revenue model, completely different set of rules in compliance, so we are very unlike them. Also, I think we started maybe a good five, six years before them so very little similarity between us and them.

Guy Kawasaki:

In these ten years of having this company and you already said you have to keep coming out with innovative products, what have you learned about keeping a startup innovative?

Nikhil Kamath:

All credit to the team. We have a great team which is constantly thinking of new stuff to put out there. The fact that we were traders to begin with helps because we kind of understand what the market might need. Also, the fact that we don't have external investors and we don't really have too many levels of hierarchy keeps us a bit more nimble and agile than somebody who has to answer to an entire boardroom and external investors before they can make a decision.

Guy Kawasaki:

Well, isn't it ironic that the company that fosters investing doesn't take any outside investment?

Nikhil Kamath:

I don't know how to look at that. I think the reason we exist, and I think the reason we have done well over the last decade is the fact that we have not looked upon ourself as a corporation, but we have looked upon ourself as traders creating a platform for fellow traders. It's a community of sorts.

With external investment, I think we would've become a corporation. We have never really done any marketing or advertising. We've never put out an ad, and we rely on word of mouth and people to like the product and talk about it. So I think we approach it less from the corporate lens and more from the community lens. Having an external investor might take away from that.

Guy Kawasaki:

Would you ever take an external investor?

Nikhil Kamath:

Not that we have thought of it. Not in the near future and probably unlikely.

Guy Kawasaki:

Well, if you don't need capital, why have the headache, right?

Nikhil Kamath:

Yeah.

Guy Kawasaki:

Do you think that investing is understanding what a company is doing, what the market is doing, or what people's sentiment about the company is?

Nikhil Kamath:

It is important to understand what the company is doing, what the fundamentals of the company are, but what moves price at the end of the day is sentiment. Very hard to read because there are so many participants, and any random set, if you were to gauge sentiment in, it might not replicate to the entirety of the company.

Sentiment is one of the hardest things to read because there are so many factors at play. Geopolitical flag factors, which central bank is printing how much money? What are commodities doing? So no one person can actually place a bet with any great degree of certainty about sentiment. But it is sentiment that moves price at the end of the day.

Guy Kawasaki:

What are the chief forms of evidence that you measure to determine sentiment?

Nikhil Kamath:

We look at things like money flow. I think more than anything, the amount of foreign capital coming into the country and who that capital belongs to makes a huge difference because often you can gauge the appetite of an investor, even though he makes a small investment, he's likely to scale it up if it is a certain kind of investor.

So, Guy, a large part of our rally recently over the last three or four months has been driven by foreign inflows. You guys in America are printing a lot of money and I think that is seeping its way into emerging economies across the world. When that tap goes off, it's a very hard thing to call. But if it does go off, I think the repercussions will be felt here and we would correct very quickly. So it would be prudent to say watching what America does with their money, the central banks in particular, is a good way to gauge sentiment going forward in India as well.

Guy Kawasaki:

Well I can understand that to gauge geopolitical sentiment, but how do you pick which equity based on sentiment? That doesn't help you pick which stock in India to invest in, right?

Nikhil Kamath:

If you stick to the large cap companies in any geography, not just in India but across the world, a better investor or a better trader, it becomes more about picking when to buy stock than what stock to buy. Because these large cap companies are pretty much always moving in the group.

If the benchmark is going up, every company in the index is going up. Some might be going up a little bit more, some might be going up a little bit less. Typically to pick market direction is probably more important to pick which particular company will do better.

Guy Kawasaki:

Do you think a good trader is a good student of psychology and behavioral economics or a quant?

Nikhil Kamath:

Psychology is probably the biggest metric in figuring out who is a better trader and who isn't. I'm a big fan of psychology, and I think being able... Nobody can really read people or read market sentiment accurately, but I think psychology helps you understand why people thought in the manner that they thought historically. In a lot of cases, these patterns tend to be cyclical. I think psychology is the one biggest differentiator in what makes a good trader versus a bad trader.

Guy Kawasaki:

Sitting in India, what is your psychological assessment of the American market right now?

Nikhil Kamath:

Wow. I think that's a tough one to call. See, I think the question, it goes even beyond America. I think you guys are printing so much money right now, but nobody's questioning that because we all have been thought and we have been bred and grown up on thinking that the dollar is essentially the currency the world will always denominate assets in.

The real question will arise when somebody really challenges that. I don't think it'll be in India, maybe it's a combination of Russia, China, Iran, and a bunch of countries who suddenly start to trade in something which is not dollar denominated, but it's a very tough thing to call. But as long as the world is buying American debt and we are kind of banking on the dollar to store assets across the world, I think it will continue to retain the predominant position it has in the last few decades.

Guy Kawasaki:

When you look at America, do you say, "Well, the sentiment there is that we have vaccines, the pandemic is coming under control, people haven't traveled, they haven't spent, they haven't visited so there's going to be an explosive economy and so the sentiment is very positive time to invest in America," or am I like smoking drugs? I'm imagining this. I'm wishful thinking.

Nikhil Kamath:

We understand things are expensive, right? Companies are expensive compared to historical averages. The multiples they're trading in, in many cases are ridiculous to say the least, but nobody knows when that will stop. Just because something is ridiculous today, it does not mean it will continue to remain ridiculous for the next ten years.

Nobody wants to really miss the boat entirely. Nobody can afford to sit out on a longer-term, ten-year trending market so I think people are buying it thinking, "Okay. I know things are expensive today, I'll get on this bus and be on it for a couple years and exit before the crash actually happens or a correction really happens." I think we all across the world understand that asset classes are inflated right now. Everything from cryptocurrencies to stock prices to real estate, most asset classes are fairly inflated relative to historical prizes today.

Guy Kawasaki:

But no one has the courage to short or very few people have the courage to short.

Nikhil Kamath:

I think a lot of people have been shorting, but they've been getting burnt out for a long, long time now. Someone smart, I can't remember who his name is now, but an American said, “Prices can remain irrational longer than you can remain solvent.” A lot of people have become insolvent by shorting and kind of schlepping through the entirety of the rally that we have just witnessed over the last twelve months.

Typically, in my experience, markets correct when this skepticism goes away. Right now we have too many skeptics around who are saying that markets are too expensive. We need to get to the point where nine out of ten people are like, "The markets went up ten percent this month. They will go up ten percent the next month and the month after that." When there is a certain degree of hubris in the market and people get a little bit cocky in a way, that's when markets typically correct and surprise people.

Guy Kawasaki:

So basically you're saying when people start believing their own bullshit, that's when it's going to correct.

Nikhil Kamath:

Yeah.

Guy Kawasaki:

You think we're close to that?

Nikhil Kamath:

I think we are. I don't know how close we are, but I think we are close to that.

Guy Kawasaki:

If you were to make an analysis about a specific company that their product sucks, the sector sucks, but the sentiment is still positive, would you still invest or do you say the fundamentals are bad, I should stay out of this?

Nikhil Kamath:

I wouldn't, but a lot of people would. I'm a little bit conservative as a fund manager or as an investor. I try to look at the glass half-empty most of the time, so I probably wouldn't. While things are expensive, I would buy what is least expensive. A lot of investors chase momentum and they don't but have a choice but to get onto companies like that.

Guy Kawasaki:

So do you think good investment is about buying right or selling right?

Nikhil Kamath:

It's about both. You need to buy right and sell right? Because at the end of the day it's also cyclical that there are up cycles and down cycles. It matters when you buy and when you sell. I don't think you have to get it perfect, but if you stay away from buying when things are too expensive, I think you'll net fine.

Guy Kawasaki:

Do you like volatility?

Nikhil Kamath:

Yeah, I love volatility.

Guy Kawasaki:

Why do you like volatility?

Nikhil Kamath:

I run a long-short fund, which kind of feeds a volatility, but outside of that, I think even as a trader, volatility allows so many more opportunities to make money in short timeframes because people become irrational when there is volatility and people will drive up the price of something either too low or too high and you get more opportunities in the market.

Guy Kawasaki:

So do you care if you make money because the market is going down? To you it's just a transaction, money's money?

Nikhil Kamath:

Yeah. Yeah. It doesn't matter. It feels the same. If I were to short something and make money or to buy something, it's the same thing.

Guy Kawasaki:

Same thing?

Nikhil Kamath:

Yeah.

Guy Kawasaki:

So then what's your feeling about cryptocurrencies? Because talk about volatility.

Nikhil Kamath:

I think they're too volatile to even have that word currency attached to them. I think they should be called something else but somebody has to remove currency from the name. I'm not a big fan, personally. I know the dollar isn't backed by anything and you guys weaned of the gold standard in the Seventies and all of that.

What we forget is there is a government backing the dollar, there is a government backing different currencies across the world. Cryptos don't seem to have absolutely anything behind them, and that makes me a bit wary. I also feel that they take power away from government and government's ability to regulate across the world. At the end of the day, we are a world ruled by politicians and governments and I don't think they will allow for this power to be taken away from them for too long without reacting.

Guy Kawasaki:

Don't you think that some of the cryptocurrency evangelists, if you will, they're saying that that's the advantage of a cryptocurrency that there's no government involved and somehow all governments are evil and they're out to screw you. So having a currency supported by people mining things is somehow better.

Nikhil Kamath:

Okay, let me look at it from another lens. Each time somebody's mining a cryptocurrency, say a Bitcoin for example, they are expending tremendous amounts of energy and carbon emissions onto the world to create something which is a token, which is actually nothing. It's terrible for the environment. I don't think it is as traceable as hard, physical currency because at the end of the day, it moves from one bank account to another and who the person is because the bank has done some kind of diligence about the guy opening an account and stuff like that.

I feel with cryptocurrency, one really bad, terrible event, like a catastrophe of sorts, which could be funded by cryptocurrency, will have a very big detrimental reaction in the price of cryptocurrency. That is true for most of the world, but some countries in Africa where inflation is like five hundred percent, they can't keep their money in currency, for them maybe cryptocurrency makes sense.

Personally, what I tell my clients and what I would rather consider doing is getting a world to maybe in a neutral, safe geography somewhere and storing physical gold, I think that's a better hedge against government than cryptocurrencies in my point of view.

Guy Kawasaki:

I have to say I'm a little surprised because I thought Nikhil was like this leading-edge Fintech kind of guy, he's going to be this great cryptocurrency expert and he's going to tell me about the great benefits, and here you are telling me it's not! That's my interpretation of what you just told me.

I've seen interviews with you where you talk about going back to the very original question that chess has rules, but within the rules there's creativity and investing has rules, but within the rules there's creativity. So have you figured out what the rules of entrepreneurship are?

Nikhil Kamath:

This will sound very counterintuitive, but often what entrepreneurs do is they fixate on one company, their holding company or their operating company and they spend all their time and effort in making that a success without diversifying, taking money out and kind of securing their lives. In material of how great a company is and how big the idea is, it's very important for an entrepreneur to have that secondary round, take out some capital, allocate it to some other thing, and diversify even a little bit because that brings a level of mental stability where you're not dependent on this one thing, that in turn makes you a better entrepreneur.

Often people would think to focus on that one company and put all your eggs in that basket is a great idea but maybe time has showed me otherwise. Having some level of diversification is good in everything, not just in entrepreneurship, in relationships, in everything, a little bit of that is good.

Guy Kawasaki:

You could make the argument that if your company offered equity and you took money off the table, you could diversify but you're not doing that.

Nikhil Kamath:

Since we are privately held, I can still take some of the profits and diversify. I don't need to necessarily sell equity. I think that works for us.

Guy Kawasaki:

So that's the rules for the entrepreneur, but what about managing the company? Have you learned some rules about managing this company and fostering innovation and keeping the wheel going?

Nikhil Kamath:

One, I feel like the old school method of having targets and reprimanding people when they don't achieve it, I don't think that works anymore. I don't think the manager or the mentor/mentee relation really works. I think people like employees in today's day need to feel like stakeholders. The more people - the promoter of a company - can give equity to and breed a sense of loyalty, not to the promoter, but to the company and the idea of the company, takes companies a long way.

Guy Kawasaki:

So do employees of your company have options?

Nikhil Kamath:

Yeah.

Guy Kawasaki:

In the United States, the way it works is there's a one-year cliff, there's four-year vesting. Is that similar to India?

Nikhil Kamath:

It is similar in India, yeah.

Guy Kawasaki:

What is your capital gains rate in India?

Nikhil Kamath:

Long-term capital gain is about ten percent with surcharge and everything else, it comes up to about twelve. Long term's definition in the Indian government's book is over twelve months. Short term is about fifteen percent.

Guy Kawasaki:

So for that two and a half percent benefit, if you exercise the option, you have to come up with the money, so then you're at risk. Why would anybody exercise the option just to get long-term?

Nikhil Kamath:

So the employee stock option route kind of changes depending on what structure you are. It's different for a private limited company, it's different for a public limited company, for partnerships. Even though the long-term capital gain rate might be ten percent, it's an extremely complex system.

For example, if a company has to pay people out, the dividend distribution tax is really high. It's like three or four times what the LTCG rate is. So it's a very hard thing to kind of explain in a short para, but the headline rate which external investors coming into India should look at is ten percent.

Guy Kawasaki:

That sounds good to me because it's much higher in the United States.

The next question is brought to you by our sponsor, the reMarkable tablet company. Unlike an iPad or many other tablets, the reMarkable tablet enables you to focus because it has a single purpose, taking notes - no email, no social media, none of the distractions of a typical tablet.

Nikhil Kamath:

I don't have very many abilities, but the one thing I do reasonably well is remain sane in panic scenarios. I think when things get chaotic, I do fairly okay. I think that I consider to be a strength of mine and I think that is very important to traders across the world because there is chaos all the time. Every now and then, something ridiculous will happen in the market with no justification whatsoever.

Personally, if you were to ask me about what time of the day or what I am doing while I do the best thinking, maybe while I'm going for a run in the gym, while I'm working out, or just before I go to bed, I think I do less thinking when I'm sitting in front of my computers than I do while I'm sitting away from them.

Guy Kawasaki:

Truly my last question, I have interviewed about seventy people for this podcast, Steve Wesner, Jane Goodall, Margaret Atwood, and I will tell you right now, you are the calmest person I have ever interviewed. If I were to write a dictionary and the answer is stoic, I would say, “See Nikhil.” So was that in your DNA? Are you doing yoga twenty-four hours a day? I mean, what makes you so calm?

Nikhil Kamath:

Yeah, a lot of people say that guy, and-

Guy Kawasaki:

It's obvious.

Nikhil Kamath:

... I think I am fairly stoic. I'll tell you the good and the bad of it.

The calmness and stoicism in a way is very good for a professional environment where there is a lot of volatility, but you take that over to your personal life and people hate that. Then you're never very happy, you're never very sad. People think you're emotionally dead in a relationship and it does not work. I think I have figured out a way to kind of turn it off and be calm all the time, I need to now learn a way to turn it on as well.

Guy Kawasaki:

There is no better way to end this podcast!

I hope you learned about the value of removing barriers, the advantages of not raising venture capital, using an analysis of sentiment and psychology to make investment decisions, the pitfalls of cryptocurrency, and the good and the bad of a calm demeanor.

My name is Guy Kawasaki, this is the Remarkable People Podcast. My thanks to Jeff Sieh and Peg Fitzpatrick, who stoically endure working on this podcast with me. Until the next episode, mahalo and aloha.

Sign up to receive email updates

Leave a Reply