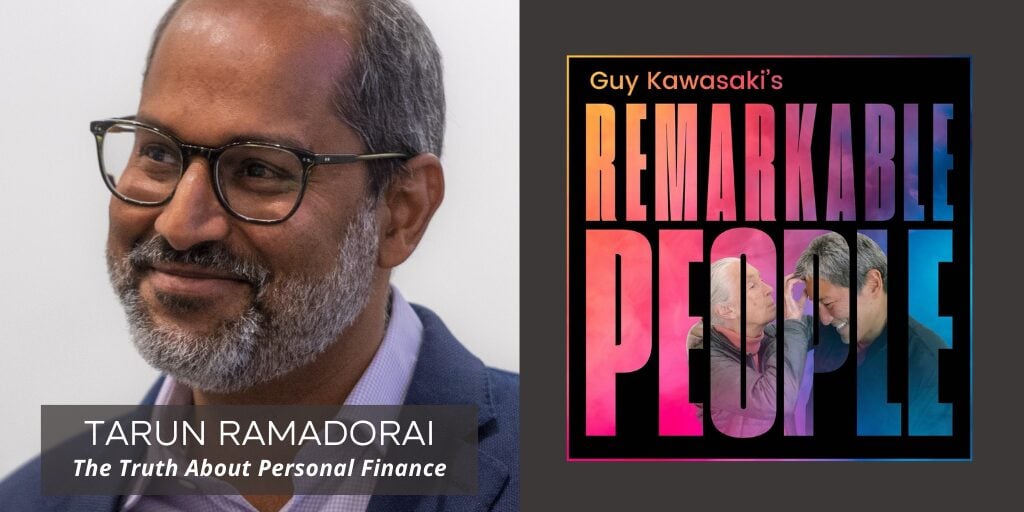

Welcome to Remarkable People. We’re on a mission to make you remarkable. Helping me in this episode is Tarun Ramadorai.

Tarun Ramadorai is no ordinary finance professor; he’s a clear-eyed critic of a system that confuses, overwhelms, and often exploits everyday people. As an academic economist and co-author of the new book Fixed, Tarun studies how humans actually make financial decisions.

In this episode, we explore why getting richer hasn’t made us calmer about money, and why even simple financial choices feel impossibly hard. Tarun explains how bias, overconfidence, and poor incentives collide in modern markets—and why many “helpful” financial products quietly work against us.

We talk about investing myths, the hidden costs of mutual funds, why index funds matter, and how compounding can either build wealth or destroy it. Tarun also challenges popular ideas like nudges, exposes conflicts of interest in financial advice, and explains why crypto and overtrading often do more harm than good.

This conversation isn’t about beating the market. It’s about surviving it—by choosing simpler, cheaper, safer financial tools that work over time. If money has ever made you feel anxious, behind, or confused, this episode will make you feel seen—and better equipped.

Please enjoy this remarkable episode, Fixing a Broken Money System with Tarun Ramadorai.

If you enjoyed this episode of the Remarkable People podcast, please leave a rating, write a review, and subscribe. Thank you!

Transcript of Guy Kawasaki’s Remarkable People podcast: Fixing a Broken Money System with Tarun Ramadorai.

Guy Kawasaki:

Good morning everyone. I am Guy Kawasaki. I guess I shouldn't assume it's morning. Our guest is actually in the evening, but I am thrilled to introduce Tarun Ramadorai. His book is called Fixed: Why Personal Finance Is Broken and How to Make It Work for Everyone.

So basically, unlike the influencers on Instagram and TikTok, he really knows how to make personal finance work. So that is a good thing.

And he's gonna express how the modern financial system is kind of structurally designed to exploit consumer mistakes and consumer weaknesses. This is a very important topic today, so let's get ready to learn about personal finance. Welcome to the show.

Tarun Ramadorai:

Thank you so much, Guy, for having me on the show and thank you for that very good introduction to the topic of our book. I think this is really an important thing.

Guy Kawasaki:

Oh, I appreciate you being on the show. Can I just express a general sort of sentiment? It seems to me in the last couple hundred centuries that we have made great progress in terms of the economic and medical health, you know, wellbeing of people that there's this really large middle class that didn't exist.

We're lifting people out of abject poverty, and yet I don't get the impression that we're any happier. Is that an accurate perception? What's going on? We're getting wealthier and healthier, but we're not getting happier.

Tarun Ramadorai:

So it's interesting that you should say that. From the perspective of the personal finance system, I think that's right. We are absolutely getting wealthier, and I think one of the great themes that we discussed in the first part of our book is that if you look at the world structure in terms of the income and wealth distributions around the world.

If you just fast forward from 1975 to 2015, just take a forty year period, we've lifted billions of people out of what we would call, as you say, abject poverty. If you were to take any definition of the absolute poverty line. Billions of people have been transported above that, many of them in Asia, which is where they were that has experienced an extraordinary wave of growth.

Now I think the point of our book is that when you move away from abject poverty, which has its own horrendous constraints that you have to deal with and you're moving into the middle class, there's a whole new set of challenges that comes along with that.

And you're entering modern financial markets, in some cases, for the first time, and you are a little bit like a deer in the headlights at that point in time. And there are many ways in which you can be predated upon by the system, which can make you very stressed out.

And as you point out, maybe quite unhappy as a result of that, even though you've experienced this enormous amount of economic growth.

Guy Kawasaki:

Why are financial decisions so hard for people?

Tarun Ramadorai:

So it turns out that if you think about the types of calculations we need to make in finance, they're very complicated calculations that involve us doing things that don't come intuitively. There's lots of decisions where we can just react in a way that actually gets us to the right answer.

If there's a wolf around, then you run in the opposite direction. And your biology is working in your favor at that point in time. But for financial calculations, you're making pretty complicated calculations. You're trying to make decisions that are gonna materialize many, many years, if not decades, after you make them, like the retirement savings decision.

You're trying to make decisions about situations where there's so much uncertainty. Should I invest my retirement savings portfolio in AI today, for example? There's a lot of uncertainty surrounding a lot of these questions.

And so this is interacting with the fact that the frame of mind we need to be to make these calculations is a very cold, calm, and collected frame of mind, but often we're not in that place.

Guy Kawasaki:

We had a guest a few months ago, and we discussed this example where, I think it was Burger King. Burger King decided to introduce a burger that was one third of a pound to give people more meat than a McDonald's Quarter Pounder. But it failed because people thought that one third of a pound is less than one fourth of a pound because three is bigger than four.

And if you can't figure out that a third of a pound is more than a quarter of a pound, I can see how you cannot figure out how to get a mortgage or make personal finance decisions.

Tarun Ramadorai:

And the thing is that some of these calculations don't come easily. There are basic financial literacy tests that many of us have structured. And the people have done great work about this in academia.

And some of those questions are as simple as, if I put a hundred dollars in a bank, paying 2 percent interest for one year, at the end of the year, will I have more than 102 dollars, equal to 102 dollars or less than 102 dollars?

And many people, if you take two other questions that are of the same level of simplicity, more people than not, combining lots of studies around the world, get those three questions wrong. The big three financial literacy questions.

Guy Kawasaki:

And using that specific example, if you sat down with the person and said, “All right, so the first year is 100 times one and two hundredths and that gives you 102. The second year is 102 times one and two hundredths, which gives you more than a hundred. Is it something that when you see that people instantly understand compound interest or is it still black magic to them?

Tarun Ramadorai:

But see, Guy, the thing that's particularly surprising about that question is you're not even asking them to do the second step of that calculation. You're only asking them at the end of one year at a 2 percent interest rate, are you gonna have 102 less or more without even getting into the compounding question.

So this is a question about simple interest, not even about compound interest. So in some ways the Burger King example does not surprise me. A lot of these things that to us come very intuitively for more than half of the surveyed population do not come as intuitively as all that.

Guy Kawasaki:

And is that the fault of the education system? I mean that people don't even have that much of a basic grasp of math.

Tarun Ramadorai:

I think for sure some of these issues with financial education have to do with the way that quantitative subjects are taught in high school, in primary school, and in various other places. Of course, there's no question about that, but I think the point is that that is a simple calculation but think about the sophistication of the calculations that we are asked to perform in the modern world.

We need to manage emergency savings, bank accounts, retirement savings, taking on a mortgage, buying or selling a home, financing education. And these are, in some cases, the complexity of these calculations is every bit as high as what a corporation is supposed to do. And yet you have individuals having to deal with these calculations on a day-to-day basis.

Guy Kawasaki:

In your book you listed the four main mistakes that people make. Would you please explain those four main mistakes?

Tarun Ramadorai:

We have this classification in the book, and I think the mistakes can be boiled down to many different simple things. One is we tend to anchor. So rather than thinking about the value of something based on a rational cold-hearted calculation about what it's worth, we tend to operate from something that's quite familiar as an anchor and then adjust away or towards that anchor.

And so that is something that, you know, is very common for us to do. For example, from my own work, when people think about what should be the price I sell my house, the very first number that comes into their head is the price at which they bought the house.

Now, the housing market could have done anything between the time at which they bought the house five, ten, fifteen years ago in some cases. It could have gone up, it could have gone down, but somehow that's the anchor that people focus on.

And even if the price has gone down 20 percent, they are just absolutely convinced that they need to get at least what they paid for it. So that's one type of mistake.

Then of course there's exponential growth bias, which is a clear problem and comes up over and over again, and we learned this during COVID, which is we realized that the cases were multiplying, but by repeated multiplication of a small number, you get a very big number.

And this is the compounding example that we talked about a little bit earlier. And yet people find that very, very difficult to make that particular calculation because it's just hard to understand, intuitively, compounding and it just catches a lot of people by surprise.

So that's another one of the examples. We can talk about those two and I'm happy to talk about some other ones as well. There are so many such examples of calculations where people find it very hard to make these kinds of decisions in a way that's reasonable.

Guy Kawasaki:

Just so I know, in that first example, you talk about pricing your house for sale is the first rational step to look at the sort of similar closings that happened in your area as opposed to what you played historically.

Tarun Ramadorai:

That is an absolutely simple way to start, right? There are more complex things you could do. You can go and try and get a sense of the market by looking at the data or trying to understand. But of course, yes, nearby houses that have similar characteristics, the price at which they sold should be a pretty good anchor.

But of course, if everybody suffers from the same problem, then all of the value could have a little bit of an issue associated with it.

The other thing, of course, is that people tend to extrapolate a lot from their personal experiences, which is another issue that comes up here as well, which is, there's always some, “Oh, my relative or my friend happened to sell a house for a little bit more than they got it for, so I should also be able to do that.”

So that then kind of turns out to be a little bit of a problem. And then that brings to light another problem that we discussed in our book, which is, how do you learn to get out of these problems?

Well, reinforcement learning is a simple way that even children learn, which is you take an action, you put your hand on a hot stove, and you only do it once because as soon as you do that, you get a stimulus that teaches you exactly how to deal with that later on and never to perform that action again.

But imagine selling a house. How many times in your life are you gonna do that, that you get the feedback from that experience to be able to learn properly?

Guy Kawasaki:

Wow. It sure sounds like the deck is stacked against us. It will take a factor of education, but of all these mistakes that people make, what do you think is the most damaging? If you had a magic wand and you say, “All right, I'm gonna eliminate this mistake, this factor,” which one would you eliminate?

Tarun Ramadorai:

I think some of the difficulties of learning are the things that, as an educator, really do trouble me the most, which is to say, you would love to believe that when we talk about education and the power of learning, that we can find a way to learn how to deal with these problems. But of course, there's a calculation that you make, you bring all of your previous knowledge into the frame.

You take the new evidence, you weight the two of those two things judiciously and appropriately, and then you come up with the right answer. But as we've just discussed, all of those processes are fraught because you might anchor, therefore you have the wrong first point at which you start.

You might overreact because of personal experiences that lead you to really get enthusiastic about information that may not be perfect. You may push too far in one direction or the other and because you're taking these actions so infrequently, you're not getting the feedback needed to make that decision better going forward.

Guy Kawasaki:

Okay, so we have all these human frailties, we have these human inadequacies. And now to make the situation worse, we also have companies who are trying to take advantage of this, right? So what do companies do when they see these human errors, this human lack of logic?

Tarun Ramadorai:

See as an academic economist, the thing that we are usually reassured by in these situations is that the power of the market will solve for these problems, which is to say that we have this trust in the market mechanisms, and broadly, we should have trust in market mechanisms because they've been a powerful force for delivering extremely high quality at quite low prices.

If you're competing on the basis of the right things, then you're getting great outcomes out of the market economy. Now, unfortunately, personal finance’s an area, as we argue in our book, where those wonderful, powerful features of capitalism are actually perverted and they're corrupted, and we call this the corruption of capitalism.

On our chapter three, “The Corruption of Finance” in particular is what we call chapter three. Now, the idea is we've just discussed how we have these human frailties. What does this mean? It means that the demands that we have for financial products and services are sometimes quite different from the demands we should have.

That is to say what we want and what we need can sometimes be two very different things. Now, if the market were competing to give us what we need, then maybe we'd get the great outcomes of having low prices and high quality. But actually, the market, unfortunately, is faced with the incentives that it will compete on the basis of the things we want rather than the things we need.

So if we misperceive the benefits of a product, if we misperceive the cost of a product, if we fail to search for a product, or if we mismanage financial products, then what happens is the capitalists supply the products that we demand, not the products that are in our best interests.

And so if you remember back in the day when, I mean there are all these ads for Lucky Strike Tobacco, where apparently doctors were endorsing these things, saying, “This will soothe your throat,” or “This will be the one that makes your life better,” and so on and so forth.

And so we're in the situation where the power of capitalism has been perverted in personal finance. And so you're right, we are in a position where there's some predation that's going on. And that's problematic.

Guy Kawasaki:

One of the most interesting examples I found in your book, and it was completely counterintuitive to me because, maybe I just bought all the bullshit, was like, when I hear people pushing mutual funds and they say, “It's a broad base mutual funds, we are gonna diversify your financial risks.

We have these experts who are making these very intellectual informed choices to get you a portfolio in our mutual fund.” And I think, Sounds good to me. And then you kind of rip that to shreds, right? So will you just tell us why mutual funds are not what you might think they are?

Tarun Ramadorai:

I think the way to think about this is that we should be comfortable with the idea that index funds have been a terrific product. And we have this wonderful wave of investment moving to passive, which in many ways has been very good for the average retail investor.

But I guess there are two things that we point to that are problematic. The first is if you fail to search, you can get ripped off even with a great product. So to give you an example, the same index that you're trying to track, whether that be the S&P 500 or something a little bit broader, like a global index.

You can get that either from a provider that provides it to you for ten basis points cost, but you can also get the same product for 1 percent or a hundred basis points cost. And if you didn't shop, you could get ripped off even with a very good product because you just didn't understand that the fee structure was so different across those two products.

Now of course, as we've just discussed, compounding works for your benefit, but compounding also works against you if you're compounding costs rather than benefits. So a 1 percent fee when you compound that is like a huge, huge drag on your total lifetime wealth. Now, to make matters worse, and I think this is maybe what you were referring to as well, there are conflicts of interest.

Which is to say sometimes the people that you are taking advice from, you need to understand how they're compensated. What is the incentive structure that is making this person propose product A rather than product B? Where are they getting their compensation from?

Are they getting it from me or are they getting it from the company that is kicking back to them for the highest commission product that they can possibly sell you some proportion of that cost, in which case the incentives are super clear? They're gonna push you the thing that is the most expensive thing, even though that's not in your best interest.

Guy Kawasaki:

Okay, if I said to you, “I want a diversified portfolio and I don't know how to pick individual stocks to do that,” what would be your advice for how I do that?

Tarun Ramadorai:

There's a very entry level answer to that and a slightly more sophisticated answer to that. The very entry level answer to that is you should pick a broad based, diversified index of international stocks weighted according to their market capitalization. That would be a simple first step that most financial economists would find uncontroversial.

But a slightly more complicated answer to that, which is not very complicated, is that the asset allocation that you have in your total portfolio should adjust according to your age and according to your wealth.

Put differently, when you're young and you have a your whole life ahead of you, you should be comfortable taking a larger proportion of stocks in your portfolio and a smaller proportion of bonds because you have a longer period of time over which that will become less risky.

And the long run expected return is gonna be high on that product. But as you get older and older, and as you approach retirement, that asset allocation has got a shift. So it moves away from stocks towards bonds, and this is what we have, and they're called target date funds. They're readily available products.

Target date funds are available at fairly low cost. Simple products, they automatically adjust your asset allocation based on your age, and that works great. Now, there's another wrinkle, which is, you can make this a bit more complicated, which is that finance theory tells you that it shouldn't just adjust with respect to your age. It should also adjust with respect to your wealth.

The wealthier you get in the product, the less risk you should be taking on. You should be dialing back a little bit on the risk at that stage, and maybe the stock bond allocation should shift back towards bonds a little bit. But that's not very hard to do.

Guy Kawasaki:

When I was reading your book, one surprise was this thing about mutual funds. Another surprise was that you highly recommended for young people that they buy stock. And I thought that was very interesting because it seems like most people would think, stock is a total crapshoot. But you're saying that if you look at the trends in stock, it is a very high return, right?

Tarun Ramadorai:

Yeah, I think it's not even about the fact that there's a very high return. This is one of those wonderful bits of financial economics where you can actually prove something to be the case, which is to say, imagine that stocks are, as you say, there's a crapshoot, there's risk associated with them.

Of course, there's risk associated with them, but the question, is that risk more often than not going to result in a payoff? Okay. Which is to say over the very long run, yes, stocks have been extremely volatile. We all know that.

But over the very long run, I think we have a pretty good sense across countries, across geographies, across time periods, that stocks outperform bonds by four to 6 percent per annum, on average, taken over a longer period of time.

What does that mean? It means that it's a positive expected value bet in the language of financial economics. What does that mean? It means that even though it's risky, every person should have at least a small amount of something that has a positive payoff in expectation.

You can prove that. And so everyone should take even just a little bit of stocks in their portfolio.

Guy Kawasaki:

A dumb question, but what is in more specific terms a little bit? Is it 5 percent, 10 percent, 25 percent, 49 percent? What is a little bit?

Tarun Ramadorai:

Yeah. What I mean by that is when I say a little bit, I guess what I'm trying to say is everyone should participate to a certain extent. Now your question is what is the extent to which we should participate? And I think what is coming out through this is that there's a fixed cost associated with participating.

If you're very wealthy, and if you have a lot of disposable wealth that you can put away, then in some sense the costs of opening up a brokerage account, any fees that you have to make, any sort of payments that you have to make, actually turn out to be a very small percentage of that total wealth.

So in that sense, one would advocate putting a substantially larger amount of one's portfolio in that.

In fact, if you had a hundred dollars of disposable wealth that you were supposed to allocate, then we would imagine that depending on your age again and your wealth level, anywhere between 80 percent of your portfolio and 40 percent of your portfolio should be in a broad-based diversified stock index is what one would normally advise.

Now this is aside from all of the other things that you might have in your portfolio, like housing and education and so on.

Guy Kawasaki:

Just as a point of clarification, because I myself do not know what the answer is, what is the difference between an index fund and a mutual fund?

Tarun Ramadorai:

An index fund is simply taking everything that's out there and then just putting it into one single bundle without necessarily taking bets about which stocks are gonna outperform relative to which other ones. So for example, if the biggest stock in the world is, I don't know, Apple for example, then you would have a very large share of Apple in the portfolio.

And then, you'd have smaller and smaller shares of all of the other things, depending in order of their size. Basically, you'd wait all of the stocks in proportion to their size, and then the index fund would simply just stick to those weights as companies went up and down and would automatically just rebalance the portfolio in that way.

A mutual fund, or a hedge fund which is an even more sort of extreme version in some sense, is just about taking views on what's going to go up and what's going to go down and doing some kind of selection in the portfolio.

And so what we would advocate is that people would not necessarily go for someone who tells you that they've got the secret special sauce, but to maybe just buy something that's a broad based, diversified index of everything.

Guy Kawasaki:

As a slice of life in your life when you go out to dinner with your friends, like when I go out to dinner with a doctor, I ask them every piece of medical advice I can. “I got this ache in my shoulder. I have headaches in the morning.”

So when you go out to dinner with people, are they constantly asking you like, “Okay, what do you think? Should I buy Apple? Should I buy Amazon? Should I buy Bitcoin?” Is your life a living hell like that?

Tarun Ramadorai:

It's almost the opposite. I remember when I was a young finance professor, people would come to me and say, “Oh, you're a finance professor. Let me tell you about my favorite theory of the way that the stock market works.”

So it's almost the reverse, which is, and in some sense, I think this sort of also exposes something of an interesting point, which is, and we refer to this in our book, which is that often people have a great deal of financial confidence.

In some cases, misplaced financial confidence. And in other cases, people are too timid. So it's almost as though we're very poorly calibrated about our financial knowledge. We're either way overconfident about our ability to really understand the financial system, or we are just so frightened of the whole thing that we do what we call going out of the frying pan into the fire.

Some people just shun formal finance altogether. They are absolutely uninterested in, they think, as you pointed out, Stocks are a crapshoot. We should not get into this. We should stick our money under the mattress.

Or we should just do family and friends type of stuff, or we should get into crypto because that's just so different from everything else. And it's not beset by the corruption of the formal financial system.

And in some sense, the argument that we make in our book is that these alternatives are all worse than actually participating in the financial system. And that's why we need this to really work well, and society needs formal finance to allocate capital efficiently.

That capital that we provide are the things that are directed to corporations to do all the great things that they do in terms of innovation at the economy.

Guy Kawasaki:

I can tell you that you better hope we never go out to dinner because if I go out to dinner with you, I know what I don't know, and I am going to pump every piece of information I can out of you. Well, that's what makes a good podcaster, right? I'm trying to get everything I can out of you in one hour.

Tarun Ramadorai:

Absolutely.

Guy Kawasaki:

So I wanna know, do you have a Hall of Fame about these countries do finance education very well, or these companies are outstanding companies that represent the best interest of their customers? Do you have a Hall of Fame? And then I'm gonna ask you for the Hall of Shame.

Tarun Ramadorai:

So I think one of the things that my co-author on this book and I have tried very hard to think about in our academic lives is a notion of international comparative personal finance. Okay.

So a different way of saying this is, it turns out that rather than thinking that some countries are great and other countries are not so great, what we'd like to be able to do is to identify best practices in particular markets around the world.

Put differently, maybe there's a place that's outstanding at having a great pension system. Maybe there's a mortgage market that is particularly good in some part of the world. So if we were to be able to identify and pick those systems that exist in different places, of course you can't just wholesale import ideas from one country to another.

You have to respect national differences. But maybe there's a way to find these gems that you can kind of put together. So to give you a few examples, the Danish mortgage market works extremely well.

So I'll give you a couple of examples. First is, one of the things about the United States and the UK and other markets like that is refinancing your mortgage can actually be quite complicated.

So when interest rates fall, then you should be getting into a mortgage product that is paying a lower interest rate, because of course, it's gonna help you manage your circumstances a lot better. Now imagine that you're a person who's fallen on hard times. Your credit conditions have deteriorated, and maybe your credit isn't as good as it used to be.

Even if interest rates fall, and this gives you an opportunity to improve your financial situation, to dig yourself out of the hole that you found yourself. In the US and in the UK, they won't let you remortgage because you have to go through a credit check.

Now, this is a little bit of a weird system because these are the people you really want to help by relaxing their financial budget constraint by giving them a cheaper mortgage, but they're precisely the people who can’t get it under that system.

In Denmark, that's not a problem. Even if you are a delinquent borrower or if you've had a deterioration in your credit circumstances, they always allow you to refinance. So that's kind of one feature of that mortgage system that's very good.

Another feature of that system that's great is that sometimes when interest rates go up relative to down, your mortgage is actually worth less in a world in which interest rates out there have gone up because new mortgages are paying more than your old mortgage.

Usually you can't do much about that. But here you can remortgage at the new market value in Denmark of the lower market value because your mortgage is now worth less, and you can just refinance at that point and take the cash out and that could be a far better situation for you.

And of course it also allows you to do the usual thing of just refinancing when its traits go down as well. So there's no asymmetry between those two cases, another great feature. Other mortgage systems have this wonderful feature called, which right now in the US is a big deal.

In the US right now, a lot of people took out mortgages when interest rates were really low, and now interest rates are six or 7 percent. So actually many people are not moving because they would have to give up their wonderful mortgage deal. And so they're locked into their houses. So what's a great feature that exists in other systems?

One is called portability. You can just take that great deal with you to the new house. You just get the lender to reassess the new house for collateral, and now you've just ported your mortgage with you.

Now this is great because you have the benefits of getting that new job opportunity in a different city or in a different house or wherever it is, but at the same time, you can take your deal with you.

You don't have to give it up. So there are many such features of the mortgage market that are great. So that's one example, Denmark. Pensions, Australia has a terrific pension system. I could sit here and really talk your ear off about that. But there are lots of situations in which there are places around the world that have done well in the way that they've designed particular systems.

Guy Kawasaki:

Can I read between the lines and conclude that the US is in the Hall of Shame?

Tarun Ramadorai:

I wouldn't say that. Look, I mean there's plenty of excellent financial innovation in the United States. Okay. And I think there are situations in which the US could improve. I'll give you another example that I think is probably useful. Actually, oddly, emerging economies have terrific payment systems.

I don't know if you've been to India or China recently. Actually paying is super easy. It's just QR codes everywhere. Everything just seamless. Transfers are happening very quickly. But in the US for example, you're still stuck with a sort of legacy system that isn't working that well. And payments are just a pain, and it just takes a while to get things going.

And so in that sense, having little encumbrance of history can actually be very helpful in just building great new technology that really helps people a lot. Another example that I think the US can absolutely improve is the retirement savings system. There are so many different types of accounts.

There's Roth IRAs, there's regular IRAs, there's 401k plans. There's Trump accounts. There's a hundred different things that are out there.

And what you really need is one account that gets opened at the point at which you join a company, and that account moves with you from place to place when you switch jobs, and you don't have to worry about all the hassle and opening up twenty-five different accounts and keeping track of them and worrying about all that stuff.

So yeah, lots of ways in which I think we can improve those systems.

Guy Kawasaki:

Okay. So going back to my theme of, I'm having dinner with you and I'm telling you right now that my listeners are thinking like, Yeah, this guy makes a lot of sense. So I would like to get your sort of quick and dirty gist advice and analysis of the most common, big decisions we need to make. Just give us like in a nutshell, this is what you should do.

So let's start with cash on hand. How much cash should I have on hand? What's the best practice there?

Tarun Ramadorai:

So a good best practice is you should have enough in emergency savings to cover at least three months of routine expenditures. That seems like a fairly simple ballpark that I think we should think about. But if you actually think about doing a calculation where you try to figure out what percentage of people actually have this kind of thing.

In the US, something like close to 50 percent of households do not have three months emergency savings. In the United Kingdom, that number is more like fifty-six or 57 percent don't have three months’ worth. And then if you move to more developing emerging economies, in South Africa for example, 90 percent of people don't have enough to finance three months of consumption.

Guy Kawasaki:

Wow.

Tarun Ramadorai:

Yeah, I know. And when you think about it, this is pretty terrifying because we were just talking about this huge transition that we've made from being in absolute poverty to moving into the middle classes. And so one of the big things that you worry about is it's so precarious, right?

Job shock comes along, a health shock comes along, something happens that's adverse. Life comes at you pretty fast as we all know. But to not be able to have that cushion that tides you over. And that’s the kind of thing that can be really damaging.

Guy Kawasaki:

Okay. Second topic, higher education. Is college worth it? Is college not worth it? Do I have to go to a great school? Can I go to a community college? Should I take out loans? What should I do about higher education?

Tarun Ramadorai:

We talk about this in the book and what we say is there are two things you should pay attention to. The first thing you should pay attention to is how much am I gonna benefit by going to university? And I think for most people, and if you look at that the data is very clear, which is that going to college is a great investment.

Okay, but, and there's always a “but,” you have to pick the course very carefully. You've gotta make sure that yes, absolutely you want to get an education because there are many great reasons to get an education, makes us better people. It enriches our lives, builds a community of friends and so on and so forth.

But there's also a dollars and cents, nuts and bolts kind of thing, that you have to think about, which is, what is the right course? How much money am I gonna make if I take on this particular degree? And that needs to be paid attention to.

So that's on the benefits side. But on the cost side, the thing you should really be paying attention to, is this a high fee paying institution or a low fee paying institution?

And that can really affect the return because the cost is gonna make a big difference to the return. And the second big thing is how do I finance this education? Okay. Do I understand the kind of student debt I'm taking on? Is it expensive or is it low cost student debt? What's the repayment plan look like on that debt?

Who's the servicer and are they a good servicer for my educational loan? And these are all of the things that we think you should think about very carefully.

Guy Kawasaki:

Okay. Next topic. Buying a house, does it make sense to buy a house anymore?

Tarun Ramadorai:

Again, this is really a question of if you buy a house, and for many people, I think, makes a lot of sense for them because personally they derive a huge amount of utility from living in their own place.

And we're not here to tell you that's not a great thing to do. You should absolutely go ahead and do whatever you like, but again, pay attention to what is the mortgage you're taking on.

Is it a fixed rate mortgage or an adjustable rate mortgage? If I take on that mortgage, have I shopped as much as I possibly can for that mortgage because this is one of the biggest financial decisions I'm ever gonna take in my life.

Okay. Apart from thinking about am I overpaying for this house or underpaying for this house, you should be doing the calculation about what have houses in the neighborhood sold for, what has been the rate of return on the housing in these places? You should be thinking about these kinds of things, but the main thing you should be thinking about is what is the cost of financing?

Am I shopping correctly for the mortgage? Am I getting the right payment? And then once I have it, am I refinancing it exactly when it's appropriate to do that? And that's something to really pay attention to.

Guy Kawasaki:

Okay. My next topic, and we've touched on this a little bit, is investing.

Tarun Ramadorai:

Now there are two components to that. One is just taking on risk and as we've discussed, anybody who has the capability to do so should take on some risk as long as it's well compensated risk, this is very important. So having a positive average rate of return over a long period of time is a good signal that this is the type of risk worth taking.

But the more important component almost for most people is retirement savings, which is a good rule of thumb is that we should have about six times the income at retirement squirreled away in the form of retirement savings. Yet most people seem very reluctant or are saving too little on average.

Many people are confused about their retirement prospects and what they believe they're going to make during retirement or how they're gonna finance their retirement. People seem very scared of annuities, even though they're very good products. And utilization is something that we absolutely recommend.

And then if you have a big house and you don't have the ability to finance it, then you should be thinking about taking on a reverse mortgage or releasing some of that home equity that you've built up over a period of time.

Guy Kawasaki:

Just a point of clarification, six times what?

Tarun Ramadorai:

Oh, six times income.

Guy Kawasaki:

So if you make a hundred grand a year, you only need 600 grand to retire.

Tarun Ramadorai:

That is a rule of thumb that most people believe is a reasonable rule of thumb, and there's lots of good calculations to support it. Now, of course, I don't say that you should have only six times. You should have at least six times.

I think that's what's very important. But if you're looking for a number, you should have at least six times. There's lots of good calculations that suggests that, but probably more.

Guy Kawasaki:

Okay. I cannot resist. I specifically want to hear what you think of Bitcoin and crypto.

Tarun Ramadorai:

Okay. Again, I think that question comes in two parts. One is what do I think about the underlying technology and does that hold promise for lots of things? And I think the answer is yes. I think we can think that blockchain technology is going to be really helpful for many things. There's many contracting solutions.

There's ways in which you can think about a distributed ledger as really helping out, for example, for housing titles or collateralization, or there's many reasons why that technology could make a huge amount of sense and really deliver great benefits. But my feelings about blockchain technology are very different from my feelings about cryptocurrencies.

Okay, and I think we need to be a little bit careful to not confuse those two things with each other. Okay. So let me give you a couple of examples for why. Okay. Now, the thing is that it almost depends on the period that you're looking at.

So today, I look like someone who is quite dissensible for not suggesting that people get into Bitcoin. We just had a big Bitcoin crash, okay? But on the other hand, the thing could go up again, and then it could go down again, and then it could go up again, and there's a huge amount of volatility, but it's just not clear what the intrinsic value of that object is.

And so in some sense, what is happening is this is one of those examples where we believe that the corruption of the financial system kind of comes into play, which is to say, when people are trying to sell you these products aggressively and marketing very aggressively, then you have to understand whose incentives these are in the best interest of.

Is it in your best interest or is it in the best interest of the person who's actually trying to sell you the product? Are these things financing transactions that you probably shouldn't want to be a part of that are on the dark web? Probably the answer is yes.

Have there been lots and lots of stories of people getting ripped off with tokens that are completely worthless at some point? Yes. Do you have the ability to distinguish between a great token and a not so great token? Probably not. So I would just, if you put all that together, it doesn't really add up to a great case for crypto, does it?

Guy Kawasaki:

To me, the investment thesis of Bitcoin is there's people who are more stupid than you that's gonna pay more. That's a very poor investment thesis in my mind.

Tarun Ramadorai:

Yeah, no, I agree and in some sense, I think, part of what we say in the book is that it's also a little bit troubling to be part of a system that your money is coming from an extractive form of capitalism where your gain is somebody else's loss. Your good deal is somebody else's bad deal.

And there's lots of cases of that strewn around the financial system that we discuss in our book. And so in some sense, that's the unfairness that we'd like to try to eliminate from the system if we can.

Guy Kawasaki:

All right. Another specific case is this, like from the outside looking in, a quick sort of overview of Robinhood is, “Oh, this is such a great deal. I can't afford to buy one entire share of Tesla so I can buy a little piece of Tesla and participate in Tesla's upside and there's no commission. Robin Hood is God's gift to a young investor.” What's wrong with that theory?

Tarun Ramadorai:

As we just discussed, one of the reasons that you should be taking on stocks is because they provide you access to the productive resources of the economy. They're basically a good bet because you're taking a bet on the productive innovation of companies in the long run, and that's been a pretty good force for wealth creation.

But the way in which you can really destroy the benefits of participating in the stock market is by doing a lot of things that we would not recommend as finance professors. One, trading a lot. Okay. Trading a lot is really a great way to just keep on squandering money because often the bets that you take are not really extremely well compensated.

You don't have a lot of information. There's so much noise that's driving stock prices around that you could actually lose more money than you gain. In some cases, there are commissions as well.

Of course the Robinhood case maybe not so much, but the money that you're kind of squandering by just having these trades go through is really coming from the overtrading that you're doing in that particular case.

And that's not so great. Of course, and early on, I don't know if you remember this, but Robinhood gamified stock trading. Every time you bought a stock, there would be a shower of confetti that came on your screen. And what is this doing? It's giving you this little jolt of happiness.

So on the one hand, look it's amusing, and it could be great, and it could be fun for people. And I have no problem with people having fun. I'm really not one of those people who's trying to stop people from having fun. You should just understand the cost of that fun, right? I think that's important.

Guy Kawasaki:

What if somebody pushes back on you and says, “What's the cost of overtrading?” It's zero commission.

Tarun Ramadorai:

The cost of over trading is that you buy stocks that go down and you sell stocks that go up, right?

Guy Kawasaki:

It's not that Robinhood profits from your over trading.

Tarun Ramadorai:

No. But then what's happening is that, again, there's a cross subsidy if you don't know what you're doing in the market, the Iron Law of Active Management, which the Nobel Prize winning economist, William Sharpe, called the Iron Law of Active Management, is that for some people to be winners in stock markets, other people have to be losers in stock markets, so there's a direct transfer.

Your losses are somebody else's gains.

Guy Kawasaki:

Okay, so I'm gonna let you off the hook because I don't wanna be that bad a dinner guest and I definitely will pick up the tab, but now one of the most interesting things I found in your book is we've had behavioral economists, we've had social psychologists on this podcast.

I found your discussion of the shortcomings of nudges so interesting. I always tell people, “Yeah, nudge is a good thing.” Like when you get your California driver's license, it defaults to, I don't know if this is true, but I think it should default to, if I get in an accident, take my body parts, I have to opt out of that, not opt into that.

So that's a nudge, right? So you're bursting my bubble here, Tarun. What's wrong with nudges and why should it be shoves?

Tarun Ramadorai:

We like nudges in many cases there. It's been a great success. There's been a lot of interesting things that have come out of that as you point out. But I think as we've had a longer period of time to evaluate the full effect of nudges, we've realized that they're not the magic bullet that they might have seen to be, and there are some hidden costs, some pretty important hidden costs.

So I'll give you just two reasons why we should not be completely cavalier about relying on nudges. The first one is some very good, very big studies that have been done evaluating lots of nudges in the field show that they're actually substantially less effective than we thought they were. Many of them just don't work.

Okay. They seem like they're a good idea. They're supposed to be this libertarian paternalism. Paternalism because the default is the right option for you, or at least determined by someone to be that way. Libertarian because you can just decide not to take it on anytime you want.

But in some sense, there's a little bit of judo going on because of the fact that your inertia is being used against you in a benevolent way apparently.

Now the first thing is, as I'm pointing out, some of these nudges just haven't been shown to work very well. And why is that? It's because if you actually look at the published research, there's a strong publication bias towards publishing the effects of very successful nudges.

But when you actually look at the effect of them when they've been rolled out into the field, they are substantially less effective than in the publications that you've actually seen, so they can be weak medicine, is kind of the first issue that we have. The second issue is that there are unintended consequences.

Sometimes this libertarian paternalism works in a way that's almost too good to be true. So let me give you an example. So one of the things that people sometimes do is that they'll enroll you in a retirement savings plan and auto deduct a certain contribution rate automatically. And that's been touted as a very good, effective nudges.

Now the problem with that is, first of all, what is the right contribution rate? Is it 3 percent? If you set it too low, then you get under saving. If you set it too high, then sometimes you get people that get into trouble because they haven't seen the fact that the money is just leaving their income every month.

And so now there's lots of studies coming out that show that people are getting into debt because they don't understand the fact that there's 6 percent being auto deducted from their income. So what does that mean? They're paying expensive debt. So net, this is a loss for them because they've just not paid attention with one eye to the thing that's going on the other side.

And okay, so that's just some examples of nudges. Now what is a shove? So I think we think of a shove, okay, is that there is something specific that we want to get to, and we'll do what it takes to get there. Okay.

And what is this? It's that we first of all want to make sure that maybe there are certain corners of the market where there's abuse occurring, where people are being sold unsuitable products. There are situations where people are getting into debt traps or trouble.

And there we are happy to advocate forceful shoves where the government comes in or the regulator comes in and says, “Listen, this just cannot be allowed to happen,” and we just stop this. So there's some intervention is certainly part of it.

Guy Kawasaki:

Can you point out some historical shoves?

Tarun Ramadorai:

Sure. For example, okay, which is, we should be, in some cases, willing to go out there and name and shame providers. Okay, so people have done this. So imagine that there's an investigation that comes out that says, I'll give you a simple example. In the United Kingdom there was a very important product called payment protection insurance.

Payment protection insurance was bundled with every credit contract that was sold in the United Kingdom for a while. Now, payment protection insurance was something that people didn't really know about.

There was just a big form. They would check a couple of boxes and off you go, and quite a large chunk was actually deducted, which was supposed to be when you lost your job or something along those lines this insurance was supposed to kick in.

In some cases, people were sold that insurance, which for years, which they paid, and they were never eligible to claim on that insurance policy in the first place. So this is a classic example where the financial conduct authority, the regulator, came in. They clamped down on this abuse, and then they forced the industry to pay billions of dollars in compensation to a bunch of people.

So that is an example of a shove, a forceful shove.

Guy Kawasaki:

I have one last question for you. I'm gonna let you off the hook. Tell me, I have asked you more questions than any podcaster has ever asked you.

Tarun Ramadorai:

I will absolutely agree with that, and I will say you've asked some very good questions as well, so thank you for doing that. This has been great.

Guy Kawasaki:

We're not the BBC here. Alright, so now I want you to explain the concept, which I loved of the Financial Starter Kit. What is in a Financial Starter Kit?

Tarun Ramadorai:

The reason we came up with the name Financial Starter Kit is we think that, anytime you start a new sport, for example, you need to have some equipment, whether that's bats, pads, cleats, helmets, protective equipment, and so on. And finance is something that you have to engage with for so many different reasons.

And we feel like people are kind of going into battle unarmed, okay? And so we really feel like there should be a suite of products that are guided by four simple principles. The first is the product should be simple. They should be cheap, they should be easy to manage, and they should be safe for people.

And essentially we think that they should be standardized, easy to manage product designs with very transparent price structures that allow people to easily comparison shop for these products.

The financial sector is allowed to offer you anything, but they should always offer you one of these very simple starter kit products, so it gives you a basis for comparison and allows you to compare across multiple providers as well. And some products are so important, like retirement savings, that it should be mandatory to choose one of these simple starter kit products.

Guy Kawasaki:

How are you gonna get something like this implemented?

Tarun Ramadorai:

Now, so I think one of the things that we're realizing is that different countries are going through different political cycles. In some places it may be more feasible to put these ideas on the table than in other places. And by the way, in some cases, governments are already doing this.

To give you an example, a very simple transactions account in Germany called the Basiskonto exists, which has a very similar form to the kind of product that we would advocate. In India, for example, there have been bank accounts that have been opened and during the PMJDY scheme, again, having the kind of flavor that we talk about.

So it isn't as though this type of thing doesn't exist in different places. It does. We just like very much to expand the set of products that enter this.

Guy Kawasaki:

How about a country where the First Lady of the country has her own meme coin? Would you say that is a part of the starter kit?

Tarun Ramadorai:

I've already told you about my views on crypto, but it's certainly the case that, look, I think one of the things that we are realizing is that sometimes change can come from unexpected places, right? Which is to say it depends on the political imperatives that people have.

And so I think as an economist who really wants to see some of these things get done, I'm happy to work with anybody who is happy to kind of work on these things as long as we get the right outcomes for a well-functioning personal finance system.

Guy Kawasaki:

All right, so I thank you for all the information.

Tarun Ramadorai:

Thank you so much.

Guy Kawasaki:

Your book was fascinating. There are many points where I said, “What?” It's completely contrary to what I thought. So that was very useful, and I thank you for being on our show. I thank you for withstanding all the pumping I'm trying to do of you, trying to get every possible thing I can out of you in an hour.

Tarun Ramadorai:

It has been wonderful and thank you so much for taking the time and for reading the book so carefully. That has been wonderful to see that, and I really do appreciate the time and effort.

Guy Kawasaki:

I think your book is a real service to people and I hope more politicians read it. Yeah. So let me just thank my staff. I wanna thank Madisun Nuismer, of course, the co-producer. I don't know where I would be without her. Jeff Sieh, also co-producer. I don't know where I would be without him.

Shannon Hernandez, sound design engineer and Tessa Nuismer, our researcher. So there's a good group of people behind me and we are on this mission to make people remarkable, and personal finance is now part of our starter kit. Thank you very much.

Tarun Ramadorai:

Thank you so much. That's wonderful.

Sign up to receive email updates

Enter your name and email address below and I'll send you periodic updates about the podcast.

Leave a Reply